During these last few years we saw an abundance of new players enter the market, capitalising on the cheap and available finance, from smaller first time private buyers through to larger syndicates and offshore groups. Those buyers who looked to diversify their portfolio with the expectation of continued strong capital growth may be feeling the pinch now interest rates have risen to their highest rate in nine years. Inversely, those who are content with steady income returns in the hope of longer-term gains are well placed to ride this wave of volatility which historically commercial property has moved in.

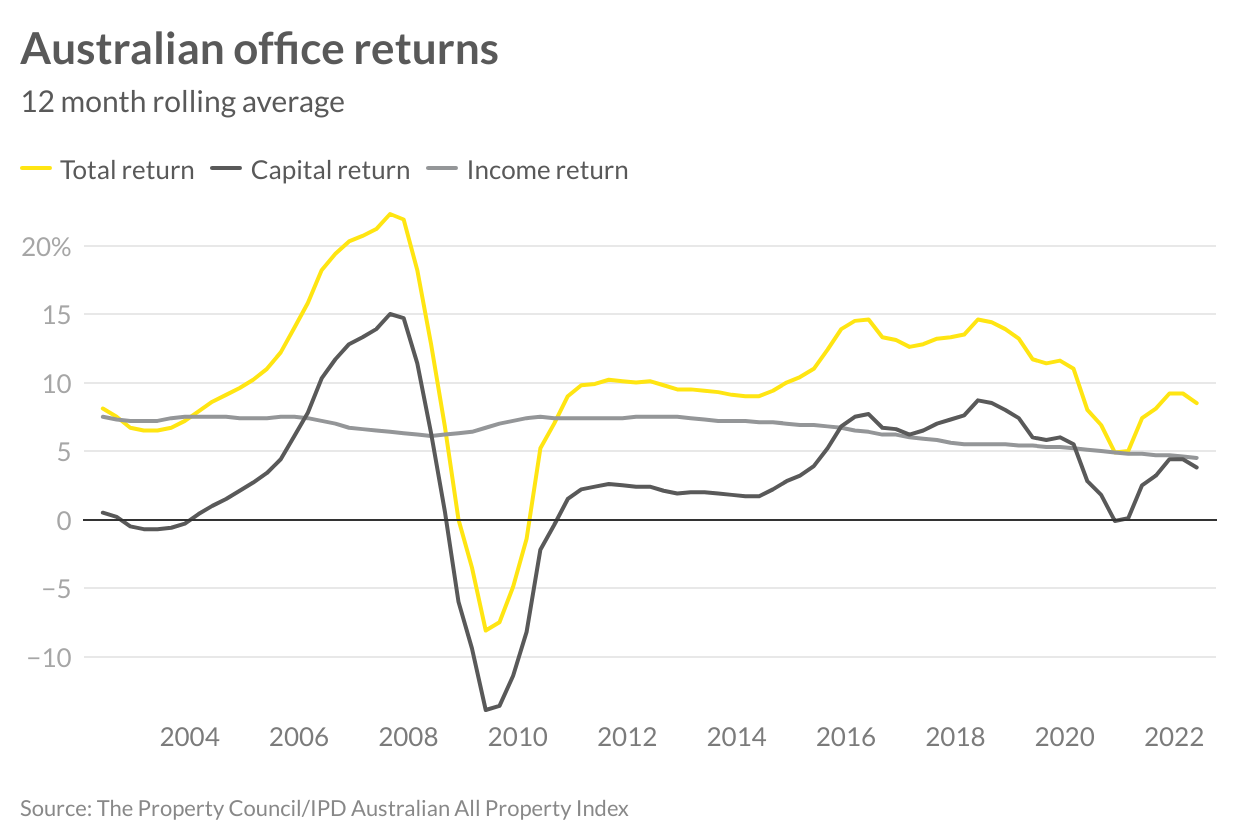

The office market was one of the hardest hit during COVID-19. The move to work from home saw many businesses reconsider their accommodation needs - either relocating, reducing or vacating their office premises. As a result, office vacancies across the country have shown an increase putting pressure on rents and capital values. Despite the change in occupancy and returns, the increased demand to purchase commercial properties saw some buyers move up the risk curve and consider office assets despite the uncertain market. This resulted in yield compression and capital appreciation despite the ongoing reduction in income return. As we enter this phase of increased financing costs, the spotlight has shone on this mismatch, and reductions in capital returns have started to emerge.

Looking across the longer term, the office market has seen much volatility moving in response to economic shocks, impacting capital and total returns. While this may result in some short-term pain for some investors, the quality returns that this asset class has enjoyed over the longer term cannot be understated. Over the past 10 years, it has returned 10.8 per cent per annum and looking back even further, including the GFC period, annual 20 year returns have also eclipsed 10 per cent.

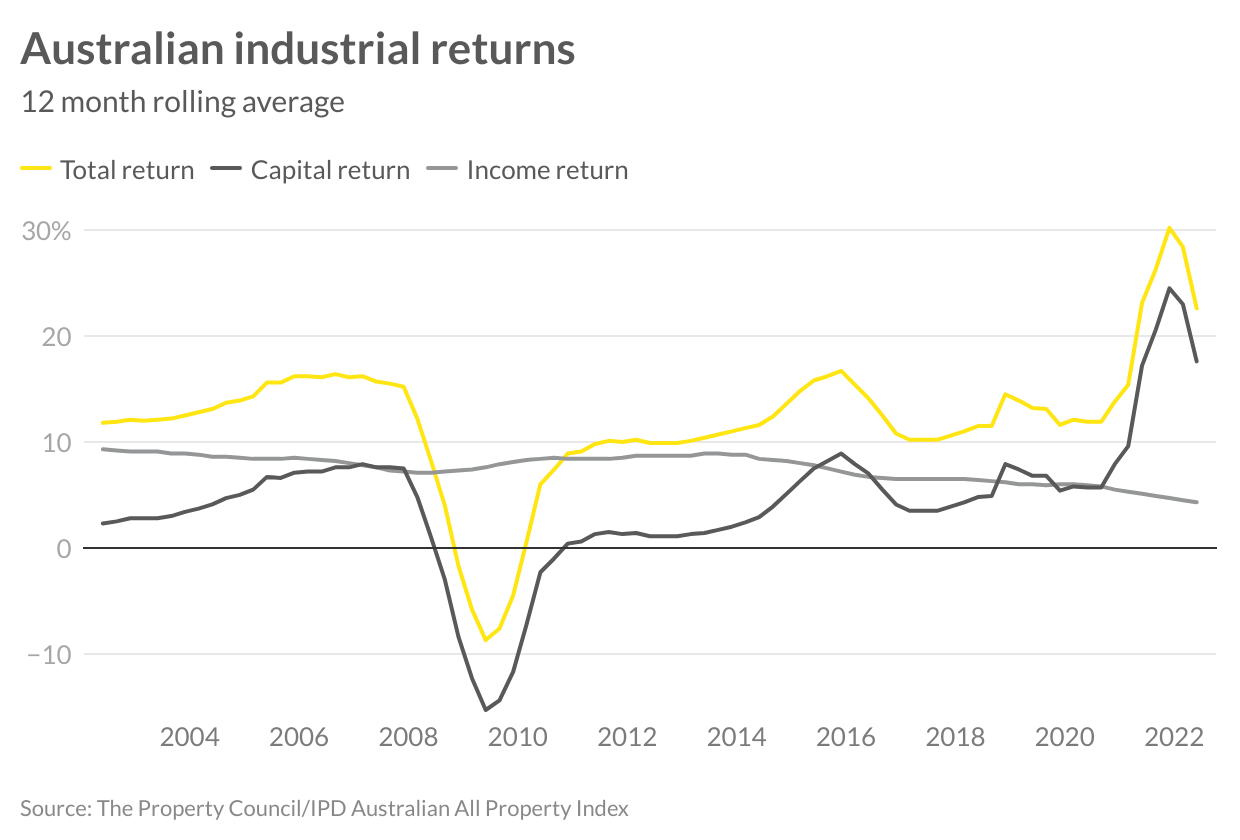

The industrial asset class has been the clear winner during the COVID-19 era. There’s been rising needs for logistic and distribution space as well as emerging small, local businesses requiring accommodation, which has ensured vacancies remain low and rents moved upward. The construction industry has slowed over the past few years and there’s been a vast increase in building costs, resulting in a lack of new supply in the market, further fuelling these results. Buyers were actively looking to invest in industrial assets, from first-time buyers through to experienced groups, with many moving towards secondary assets in the quest to secure an industrial property. As a result, we saw annual total returns peak at 30.2 per cent in December 2021 - a rate well in excess of any previous highs for this market.

While the mismatch in supply and demand ensures income growth will continue for this asset class, the growing interest rates will put a cap on acceptable yields for industrial property in the short term. Industrial has proven to be an outstanding performer and has moved from what was considered as a secondary asset class to a premium one, given the changing way in which our community interacts with industrial property. Total returns over the last five years have hit 15.6 per cent per annum and 14 per cent per annum over the past 10 years, highlighting the longer-term attractiveness of this asset class. Considering the downturn during the GFC, total returns - even over a 20 year horizon - still achieved 12 per cent annually, highlighting the quality, longer-term opportunity on offer for industrial assets.

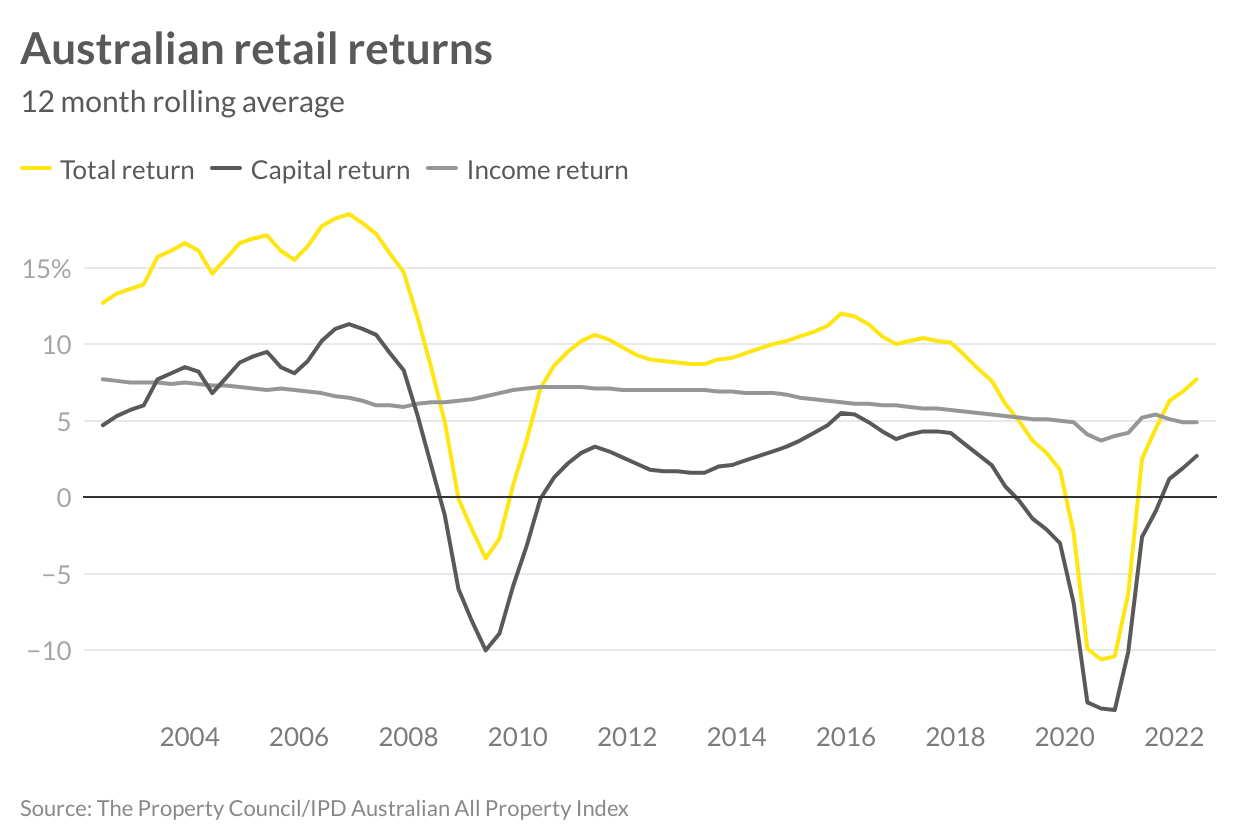

The retail market has been one of the harder hit asset classes over the past five years, even prior to COVID-19 competition from online retail. This raised the question of the viability of many retail assets, pressuring investment returns. We’ve seen, however, the reinvention of many retail centres and strip shops over the last few years, capitalising on the growth in alternative uses such as medical and childcare. These spaces have also been creative in the adaptation of customer experience via entertainment and food offerings. Investment has rebounded again, creating new benchmarks in yields, with assets with development potential now viewed in a different light. While this market has endured the greatest volatility of the major commercial markets, returns continue to be positive and investment demand up albeit at the right price.

Over the past 10 years, retail property has been under the microscope, and during the last few years not enjoyed the same level of investment demand as other commercial real estate. Despite this, total returns still averaged six per cent per annum, while over the longer term (20 years), total returns achieved nine per cent annually, highlighting that commercial assets are a long-term investment play.